I'm Still Long

Market Rewind: June 29-July 2, 2026

The Dow printed an all-time high, the chips dropped quite a bit, and the jobs print came in soft. A holiday-shortened week that clarified the regime we’re now trading in.

Also in this article: the memory laid out E2E, and a new recurring feature — From the Filings — on what AAOI’s fourth-fab 8-K actually says.

It was an interesting week to say the least. I have many takeaways from this past short week. So, let’s dive in.

Quick disclaimer: I am not a financial advisor so nothing from this article should ever be considered financial advice. Yes, I do own stakes in multiple companies I will talk about in the article. As always, DYOR/DD, and best of luck to you. If anything below is wrong, outdated, anything at all, please let me know. I dig through tons of news, articles, sitting in VS Code building graphs, so please, let me know gracefully. Though, I did not build any in this article. But seriously, if anything is wrong, let me know!

I. The Tape

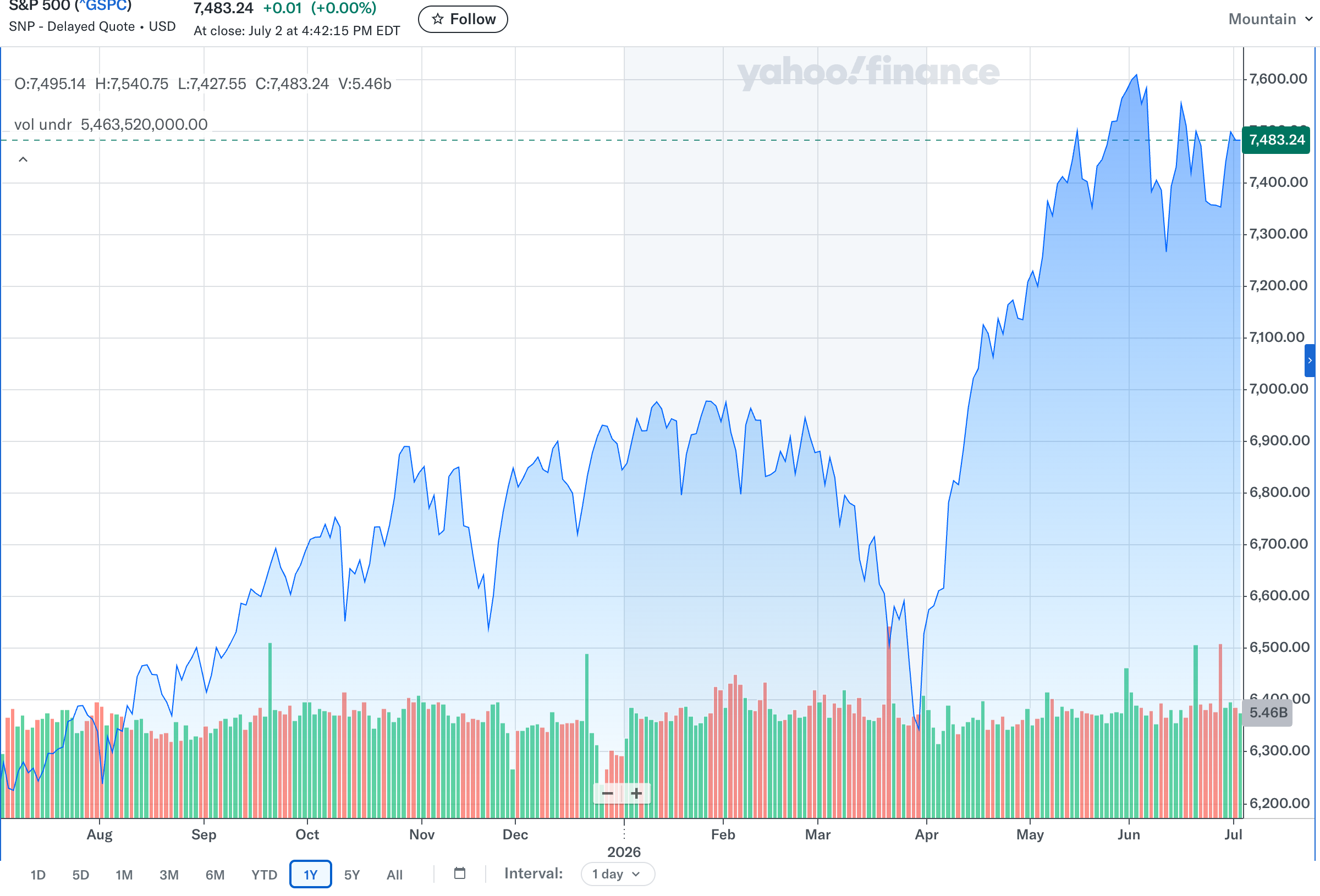

The headline indices undersell what happened this week. Here is where things closed on Thursday, July 2:

Dow Jones: 52,900.07 — a fresh ATH, up 1.14% on the day. Apple, McDonald’s, and Disney led it.

S&P 500: 7,483.24 — roughly flat on the week, just off its June 2 record of 7,609.78.

Nasdaq: down 1.61% on Thursday. This is where the pain lived all week.

Russell: lagged — small-caps couldn’t hold a bid, with rate sensitivity showing.

SOX: 12,626.22 — down 5.44% on Thursday and down about 11.4% over two sessions.

VIX: 15.85 — low, because this was a rotation, not broad de-risking.

10Y: ~4.48% — no cuts priced.

WTI Crude: ~68.50 — drifting into the long weekend. (will go lower, IMO)

Now, the market did not fall this week. It rotated out of the parabolic semis names and into cash-flowing companies.

I own semis, so this week was rough. It changed the tape, not the thesis.

II. The Headlines

Let’s go in order here:

Monday, June 29

Mega-cap tech and the hyperscalers snapped back after a soft prior week. The Nasdaq rose intraday, alongside the S&P and Dow. Nothing fundamental drove it — this was positioning and quarter-end window dressing into the strongest quarter in years. The froth was still fully intact.

Tuesday, June 30

Q2 2026 closed as the best quarter for US equities since the 2020 pandemic rebound. The Dow moved up a modest amount. Moves on the day were muted, however. This was the high-water mark; the mood cracked next session.

Wednesday, July 1 — four things moved the tape

The EU-US trade deal took effect. The Council of the EU adopted the enacting regulations, so as of July 1 most EU imports into the US carry a 15% tariff, while the EU drops duties on US industrial goods and opens preferential access for select farm and seafood products. Markets read a known 15% as better than unknown escalation — a mild positive for large-cap multinationals with pricing power, which is to say the Dow.

USMCA talks failed. USTR Greer confirmed the US could not reach agreement with Canada and Mexico. This does not end the pact immediately — it drops into an annual review process running up to 10 years, expiring in July 2036 only if never renewed. A headline risk, not a cliff. Autos and industrials wobbled.

BofA flagged “bubble risk” in the AI trade (alright, cmon). BofA stopped short of calling a top but told clients to reintroduce valuation discipline after a parabolic run. Chips sold off throughout the day. Now, when will BofA get it? Not sure… lol.

Meta went the other way — and hard. Two things landed. First, Zuckerberg raised Meta’s 2026 capex guide to $125-145B (from $115-135B), explicitly citing higher component pricing — read: memory — plus competition for land, power and labor. Second, and the part I found most interesting: “Meta Compute,” a plan to rent Meta’s AI compute to outside companies — on-demand GPU clusters, hosted Llama models (and its new closed-weight Muse Spark), and agent tools — reportedly undercutting AWS and Azure by 20-30% on GPU-hours using its own MTIA silicon. The stock ripped 7.56% on the day. I get into why this one actually matters down in the selloff section.

The Dow still closed at a record. Money left the crowded semi trade without leaving the market (they will be back, soon, IMO).

Thursday, July 2

June jobs report: nonfarm payrolls came in at +57,000, a large miss versus the ~115K consensus and down from a revised 129K in May. April and May were revised down a combined 74K. The unemployment rate fell to 4.2%, but for the wrong reason — labor-force participation dropped 0.3 points to 61.5%, the lowest since March 2021. Average hourly earnings rose 0.3% MoM to 37.64.

The market’s read: a weak but not collapsing labor market quieted the rate hike conversation (@BofA, hear that?). Treasuries caught a small bid and the 10Y hovered near 4.48%.

Intel headline: HSBC raised its Intel price target to $200 from $100, reiterating Buy. I loved this.

Friday, July 3

Markets closed for Independence Day.

SK Hynix reportedly slowed its HBM capacity expansion — read by some as a demand-signal scare, by others as supply discipline.

The memory-cycle debate got even louder. The question is whether SK Hynix pacing HBM means disciplined supply or the first crack in demand. The bull case also runs through NAND — inference turning it into a scarce resource (model weights, KV-cache offload, checkpoints, data lakes, nearline).

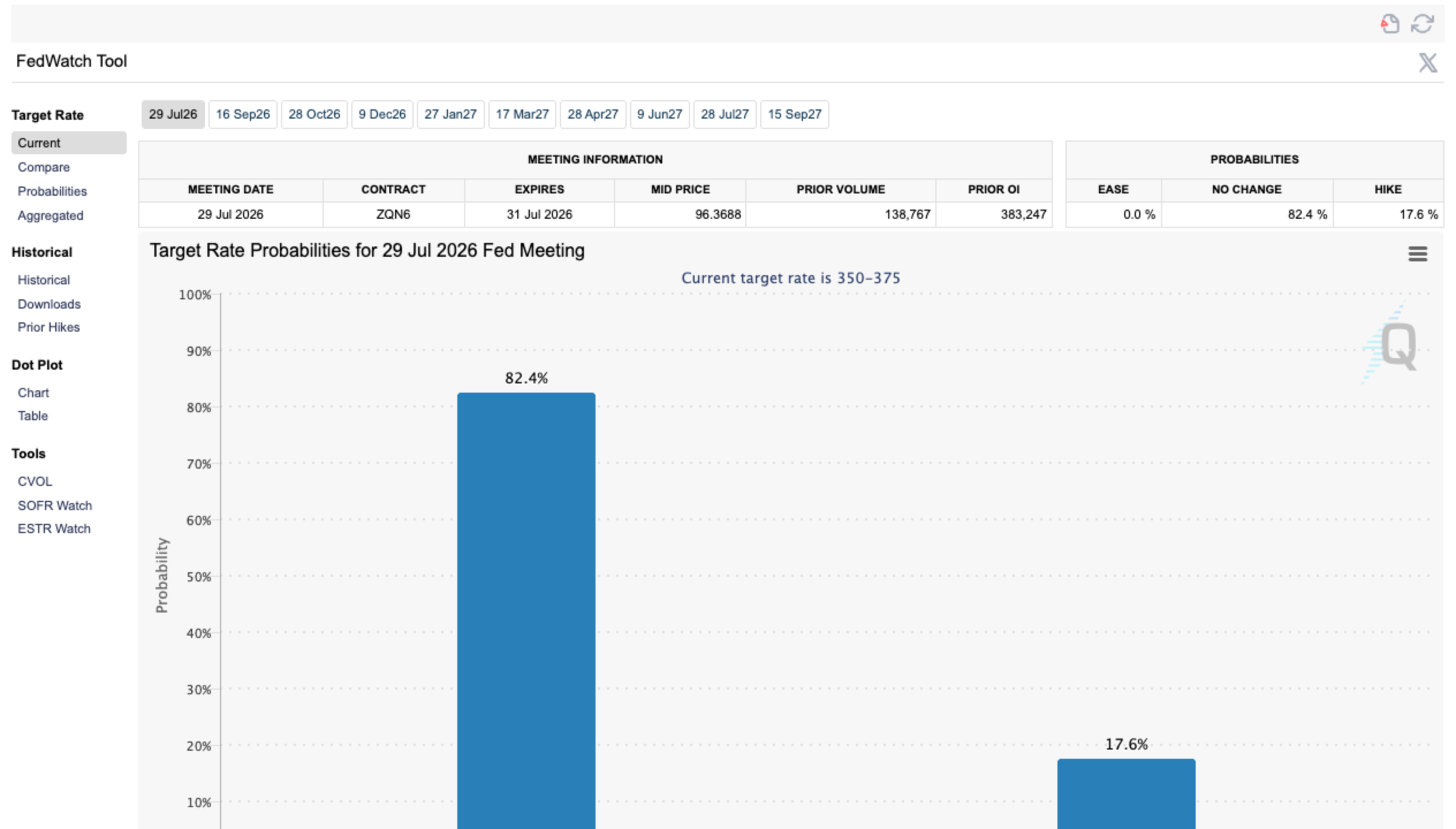

III. The Fed

Warsh ran his first FOMC on June 17, and the committee held the funds rate at 3.50%-3.75% for a fourth straight meeting — a unanimous hold. The shift wasn’t anything Warsh said. He pointedly declined to signal the July decision and didn’t even submit his own rate projection, a hawkish tone. He called inflation “too high” and promised the Fed will “deliver price stability” — but he did not commit to hikes. What moved was what his colleagues penciled in. (And note: at the ECB forum on July 1 this week, Warsh actually said inflation risks and expectations have come down — a quietly dovish tell that gets ignored.)

The dot plot I am speaking about:

Nine of Warsh’s colleagues now project at least one 25bp hike by EOY, six of them two or more — a sharp reversal from March, when no one penciled a hike and the committee’s median was a cut.

The median end of 2026 fund rate moved up to about 3.8% from 3.4%.

The statement kept inflation “elevated” on supply shocks, including energy, and Vice Chair Bowman has said a hike may be warranted if those pressures persist (fun fact from me, they won’t).

The futures market agrees. As of July 2 close, CME FedWatch priced the July 29 FOMC meeting at 0.0% for a cut, 82.4% for no change, and 17.6% for a hike, from the current 3.50-3.75% target.

With all of this being said, it is important to note that as of now, the discount rate is no longer a tailwind, this is why the soft jobs print rallied stocks, and tariffs are now a supply-side inflation input the Fed is watching.

However, my take is that we do not see a Fed hike in July. The labor market is cooling — 57K, negative revisions, sub-62% participation — and Warsh is not going to tighten into visible payroll deceleration on his first real decision. I also do not think we see rate hikes this year.